Market Update – Precious Metals and Mining Equities

Recent market movements have led to a corrective phase in both gold and silver prices after the strong rally that took place in January, when gold traded above USD 5,400 per ounce and silver exceeded USD 116 per ounce. Mining equities have followed this pullback, declining alongside the underlying metals.

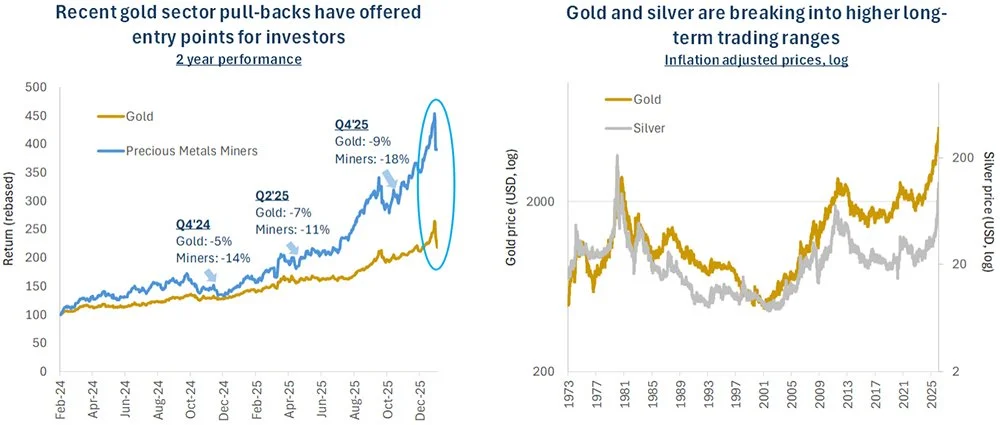

From a long-term investment perspective, such periods of consolidation have historically offered constructive entry points within the precious metals cycle. Corrections of this nature often help rebalance market positioning and bring valuations back to more attractive levels ahead of the next upward phase.

The recent weakness appears to have been driven primarily by profit-taking. Subsequent market commentary pointed to the likely nomination of Kevin Warsh as the next Chair of the US Federal Reserve as a potential explanation for the correction. In our view, this narrative reflects a short-term market interpretation rather than a genuine change in underlying fundamentals.

Regardless of the individual appointed, structural constraints linked to elevated US deficits, rising interest payment burdens, and long-term fiscal imbalances are unlikely to be materially altered. As a result, the broader environment of negative real rates and currency debasement pressures remains intact, a backdrop that continues to support the long-term case for precious metals.

Our positive long-term outlook for the precious metals sector remains intact, as the structural drivers underpinning the bull market in gold and silver remain firmly in place. Continued geopolitical uncertainty and macroeconomic volatility reinforce gold’s role as a strategic reserve asset, particularly for central banks. At the same time, persistent inflationary pressures and the structural challenges associated with elevated levels of US federal debt point toward a prolonged environment of financial repression. Historically, such conditions have supported investment demand for precious metals as a means of preserving purchasing power. In parallel, industrial demand dynamics are also favourable, notably the growing use of silver in photovoltaic solar technologies, while supply conditions for both gold and silver remain constrained.

Looking back over the past two years, similar pullbacks in gold, silver and mining equities have repeatedly proved to be healthy pauses within a broader upward trend. These corrections have typically been shorter and less severe than many market participants anticipated, with prices recovering as underlying fundamentals reasserted themselves. During the previous trough in gold prices in October 2025, the market took just 19 days to reach its low. A sharper correction in the current episode could, therefore, be consistent with a faster subsequent recovery.

In this context, Apis Asset Management is using the current market weakness to position portfolios for the next phase of the metals and mining cycle. We continue to see attractive opportunities across the precious metals mining sector, where companies are benefiting from improved margins, disciplined capital allocation and tighter cost control, leading to stronger profitability. Beyond precious metals, we are also identifying value in other segments of the metals universe that may have been indiscriminately affected by the broader market sell-off.

With mining equities appearing attractively valued, both in historical terms and relative to underlying metal prices, our approach remains focused on selective, active stock picking. This disciplined process is designed to navigate periods of volatility while capturing long-term upside potential as the fundamental backdrop continues to improve.

We remain at your disposal for any further information.

Kind regards,

Apis Asset Management