Market Update – Precious Metals and Mining Equities

The gold sector has experienced a notable correction over the past week, which may raise questions regarding its safe haven role, particularly in the context of ongoing geopolitical tensions in the Middle East. While market conditions remain uncertain, we believe this recent dislocation offers an attractive entry point for disciplined investors looking to build or reinforce exposure to the sector.

In response to the recent sell-off, the Apis Asset Management team has acted swiftly to reposition both our Precious Metals and Electrum strategies, with a view to navigating near-term volatility while preparing for the recovery we expect as underlying fundamentals reassert themselves.

In our view, the recent pullback in gold has been primarily driven by short-term macroeconomic factors and liquidity pressures, rather than any deterioration in the long-term investment case. A sharp rise in US real yields, combined with a stronger US dollar, has weighed on gold, silver and mining equities. This movement, which has brought gold prices back to levels last seen in December, has likely been amplified by profit-taking following the sector’s strong performance in early 2026. Gold mining equities have similarly retraced.

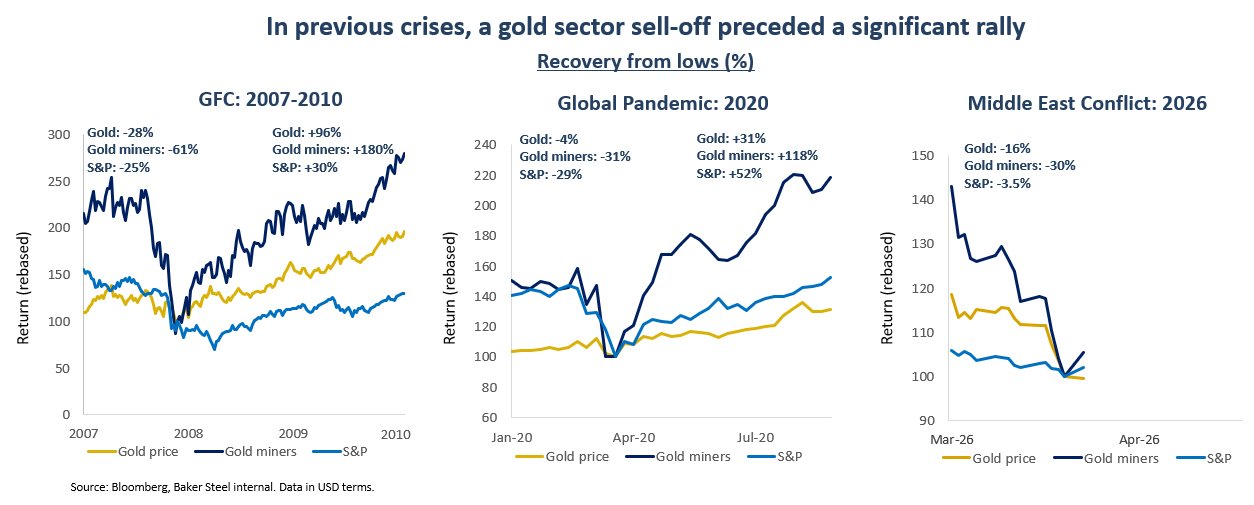

Such corrections are not uncommon within broader bull markets. History offers several relevant precedents. During the Global Financial Crisis in 2008, as well as during the market stress of the 2020 pandemic, gold and precious metals miners experienced significant drawdowns before entering strong recovery phases. In both instances, mining equities led the rebound, outperforming both physical gold and broader equity markets.

In previous periods of market stress, gold and gold mining equities experienced short-term drawdowns before entering strong recovery phases.

We believe the current environment presents a comparable setup, as the fundamental backdrop for the sector remains intact. While short-term volatility may persist, particularly if broader equity markets weaken, current geopolitical developments are increasing the risks of inflation, stagflation and widening fiscal deficits. The growing burden of US federal debt, combined with political pressure to maintain accommodative monetary conditions, points towards a regime of financial repression, especially if real rates turn negative. In such an environment, gold and precious metals continue to play a key role as stores of value.

At the same time, central bank demand remains supportive, while structural demand for metals such as silver (particularly linked to solar photovoltaics) continues to strengthen. Combined with constrained physical supply, these factors underpin a robust long-term outlook for the sector.

Against this backdrop, we have used recent market weakness to selectively increase exposure to high-quality, undervalued mid-cap gold miners, while carefully reassessing risk profiles across the portfolio. We have also rotated towards companies less exposed to potential energy supply disruptions and are actively engaging with management teams to assess their ability to manage rising production costs and potential supply chain pressures.

We remain confident in the outlook for gold and precious metals equities and believe current conditions are laying the foundations for the next phase of the cycle. Despite potential cost pressures, the sector continues to benefit from strong margins and disciplined capital allocation. More broadly, we also see emerging opportunities across industrial and speciality metals impacted by the current environment.

With mining equities trading at attractive valuations, both on a historical and relative basis, we continue to identify opportunities through a disciplined and selective investment approach.

Thank you for your continued trust. Should you wish to discuss recent market developments or portfolio positioning in more detail, we remain at your disposal.

We remain at your disposal for any further information.

Kind regards,

Apis Asset Management