Strategic metals : The return of real assets in a fragmented world

A private wealth perspective on industrial sovereignty, energy security and the re-rating of critical resources.

A private wealth perspective on industrial sovereignty, energy security and the re-rating of critical resources.

For private wealth investors and allocation professionals

I. STRATEGIC INTRODUCTION

The role of metals in the global economy is changing in nature. Long regarded as mere industrial inputs, whose prices fluctuated in line with macroeconomic cycles, they are now taking on a dimension that brings them closer to strategic assets than to conventional commodities. This transformation is not cyclical. It reflects a profound recomposition of the economic, technological and geopolitical balance of power, in a world that has become structurally more fragmented.

Three forces are converging to reshape this landscape. First, structurally more intense demand, driven by the broad-based electrification of economies, the expansion of artificial intelligence, the transformation of energy systems and the modernisation of defence capabilities. Second, constrained supply, inherited from a decade of chronic underinvestment and now subject to geological, operational and political bottlenecks. Third, a new political economy in which states are once again becoming direct actors in the securing of supply chains, through subsidies, equity stakes, strategic stockpiling and export controls.

Added to this threefold sectoral dynamic is a macroeconomic environment that reinforces the appeal of hard assets. Sovereign debt levels in developed economies, the persistence of inflationary pressures, the prospect of prolonged fiscal dominance and the slow erosion of the unipolar currency system constitute a favourable backdrop for real assets, whether precious metals, industrial metals or listed mining equities.

For the wealth investor, these developments open a field of reflection that goes beyond conventional cyclical analysis. It is no longer simply a question of anticipating a cyclical rebound in commodities, but of integrating critical resources into a long-term strategic allocation logic, structured around industrial sovereignty, energy security and the preservation of real purchasing power.

II. WHY STRATEGIC METALS ARE BECOMING CENTRAL AGAIN

Demand driven by major technological transformations

The return of metals to the heart of the global economy is explained first and foremost by the scale of the needs generated by the technological transformations currently under way. Electrification is no longer a sectoral theme confined to electric mobility or renewable energy: it now runs through the whole of industrial chains, from transport infrastructure to distribution networks, from buildings to data centres.

Artificial intelligence provides a particularly compelling illustration of this dynamic. The proliferation of data centres and intensive computing infrastructure is driving accelerated growth in electricity demand, a rising share of which operators are seeking to direct towards renewable or low-carbon sources. This additional demand in turn requires more copper for cabling, more aluminium for structures, more nickel and cobalt for storage, and more uranium for baseload power generation.

The orders of magnitude are significant. By 2035, copper demand is expected to rise by around 29%, aluminium by 23% and uranium by 29%, while lithium demand could increase more than fourfold. In China, the world’s leading industrial market, copper and aluminium consumption linked to clean technologies is expected to exceed demand from the traditional construction sector as early as this year, marking a structural shift in the drivers of consumption.

Rearmament as a structural demand factor

Added to this civilian dynamic is a strengthening of demand linked to military needs. Modern defence systems are highly metals intensive, requiring copper for electronics, tungsten for munitions, nickel for aerospace applications and rare earths for the permanent magnets that equip advanced guidance systems. The economic asymmetry of contemporary conflicts (expensive interceptor missiles set against low-cost drones) also weighs on inventories and intensifies pressure on supply chains.

Recent conflicts in the Middle East have confirmed this trend. The multi-year rearmament programmes launched across most of the major Western economies, as well as in Japan, South Korea and India, extend this underlying trend. Security of supply for critical metals is now addressed, in a number of strategic doctrines, on the same footing as energy security was in past decades.

Structurally constrained supply

In the face of this demand, the mining sector’s productive capacity is running up against increasingly tangible limits. Project development timelines have lengthened: a new copper deposit now requires nearly eighteen years to reach production, compared with around twelve years in the mid-2000s. Ore grades are declining across most legacy deposits. Permitting processes have become more cumbersome. Environmental and social constraints have tightened. The cost of capital required to launch new projects, in a context of durably higher long-term rates, represents a further headwind.

The logical consequence is that supply deficits are expected to emerge by 2030-2035 for several strategic metals, notably copper, cobalt, uranium and lithium. These imbalances should provide durable support for prices and create an environment favourable to producers with quality assets, capital allocation discipline and exposure to the most constrained metals.

III. THE GEOPOLITICS OF SUPPLY CHAINS

Geographic concentration and asymmetry of dependencies

One of the most striking features of the current landscape lies in the extreme geographic concentration of critical metals supply chains. Both mining operations and refining and processing capacity are concentrated in a small number of jurisdictions, often outside the OECD, which creates asymmetric dependencies for Western economies.

China occupies a dominant position across the entire value chain. It accounts for a majority share of global rare earths refining, controls a substantial fraction of lithium, graphite and tungsten processing, and plays a central role in the processing of copper, nickel and aluminium. This dominance stems not only from geological advantages, but from a strategic effort spread over several decades, combining industrial investment, energy policy and vertical integration.

Other actors hold critical positions in specific segments. Indonesia now dominates the nickel sector, with a majority share of global production and rapidly growing processing capacity. The Democratic Republic of the Congo accounts for a decisive share of cobalt supply. Australia remains a key supplier of lithium and bauxite. Kazakhstan, Canada and Niger play a central role in the uranium cycle. This distribution creates a map of dependencies that does not necessarily align with traditional diplomatic alliances.

Vulnerability of trade routes

Added to this concentration of production is the fragility of the maritime routes through which these flows transit. The strategic chokepoints (Hormuz, Malacca, Bab el-Mandeb, Suez) constitute critical passage points whose disruption can significantly affect supply. The conflict in the Middle East has been a reminder that the risks weighing on these logistical corridors are not theoretical: they translate into higher marine insurance costs, longer delivery times and, in some cases, production stoppages.

The example of aluminium is instructive. The Persian Gulf concentrates around 9% of global primary production capacity, the bulk of which transits through the Strait of Hormuz. Any prolonged disruption of this route can place several million tonnes of production at risk, with immediate consequences for international prices and the stability of downstream supply chains.

Export controls as a strategic weapon

The trade policy toolkit has also evolved. Export controls, once marginal in the mining sector, have become a central instrument. China has made increasing use of them in recent years, successively restricting exports of gallium, germanium, antimony and graphite, followed by processing equipment. Signals indicate that restrictions could extend to rare earth refining technologies themselves, which would constitute a major qualitative step change in the instrumentalisation of critical chains.

These decisions are in keeping with historical precedent. Chinese restrictions on rare earths over the past decade had already disrupted global markets and led several economies (notably the United States, Japan and Australia) to engage in diversification strategies. The repetition of such episodes, against a backdrop of intensifying technological rivalry, reinforces awareness of the structural vulnerability of Western economies.

IV. THE RETURN OF THE STRATEGIC STATE

The United States: from a financing approach to direct equity participation

Faced with these dependencies, Western economies are redeploying their industrial policy toolkit with an intensity unseen for several decades. The United States has led the way. The Inflation Reduction Act of 2022 laid the first foundations of massive support for strategic value chains, combining production tax credits, domestic content requirements and reshoring incentives. While certain provisions have been adjusted following later political changes, the general architecture of the framework has remained foundational.

The next step was taken with the One Big Beautiful Bill Act, which for the first time establishes a budgetary envelope explicitly dedicated to the extraction, refining and processing of critical minerals. The framework provides for up to USD 5 billion of direct investment, USD 500 million in credit subsidies capable of mobilising up to USD 100 billion in loan guarantees, and USD 3.3 billion for long-term offtake contracts. Added to this is Project Vault, which aims to establish a USD 12 billion strategic national reserve covering rare earths, lithium and nickel.

Beyond the new legislation, existing frameworks have been repurposed. The Defense Production Act, the Export-Import Bank, the Development Finance Corporation and even certain components of the CHIPS Act are now mobilised to support mining projects, both at home and abroad. Cumulative commitments by the current US administration are estimated at approximately USD 18.6 billion, spread across around sixty projects.

The most notable change lies in the nature of these interventions. Washington is no longer merely lending or subsidising: the US government now takes direct equity stakes in certain mining companies. Lithium Americas’ Thacker Pass project, initially supported by a Department of Energy loan, has evolved into a direct equity participation, alongside a joint venture with General Motors. MP Materials, operator of the only active rare earths mine in the United States, has been the subject of a USD 550 million strategic investment by the Department of Defense. This shift from a financing approach to direct equity participation marks a historic break with the non-interventionist doctrine that had previously prevailed.

A broader Western mobilisation

This movement extends well beyond the American context. The Pax Silica initiative, conducted under United States leadership, aims to structure a Western supply chain for critical metals linked to artificial intelligence, valued at USD 1 trillion. The Critical Minerals Partnership signed between the United States and Australia in 2025 mobilises USD 8.5 billion in project financing, in direct response to Chinese pre-eminence.

The European Union is advancing along complementary lines, structured around the Critical Raw Materials Act and the RESourceEU initiative, whose ambition is to create a European centre for monitoring, joint procurement and stockpiling of critical raw materials. France, Germany and Italy are driving enhanced coordination. The United Kingdom is exploring strategic stockpiling arrangements via NATO and dedicated national frameworks.

In Asia, Japan and South Korea already have reserve systems managed by public authorities and continue to expand their network of international partnerships. India has launched its National Critical Mineral Mission, while bilateral agreements between Japan and Australia complete the framework.

A new political economy of resources

Taken together, these developments point to a paradigm shift. For several decades, the dominant doctrine rested on the efficiency of global markets, international specialisation and cost optimisation. The pendulum has shifted: resilience, security of supply and control of the strategic nodes of the value chain now take precedence over pure optimisation. The implications for markets are substantial, since this new political economy introduces a durable geopolitical risk premium into price formation, and structural support for the valuation of strategically positioned assets.

V. PRIVATE WEALTH PERSPECTIVE

The return of real assets to allocations

For the wealth investor, the context described calls for reflection that goes beyond the usual cyclical reading. Several forces are converging to place real assets back at the centre of long-term strategic allocations.

The first is the inflationary backdrop. The US M2 money supply has expanded by around 48% since the beginning of 2020, meaning that approximately one third of the dollars currently in circulation have been created over a very short period. Added to this monetary expansion are the inflationary effects of tariff policies, supply chain tensions and the energy crises linked to recent conflicts. In such an environment, assets whose supply is by nature constrained (precious metals, critical industrial metals, land resources) retain a notable relative advantage over purely financial assets.

The second concerns sovereign debt levels. The public debt-to-GDP ratio in the United States is approaching 122%, compared with 32% at the end of the 1970s. Federal debt servicing costs now exceed USD 1 trillion per year, around 19% of federal revenues, and exceed the defence budget. This configuration creates a structural constraint on the room for manoeuvre of central banks and increases the likelihood of prolonged fiscal dominance, in which monetary policy remains accommodative to support fiscal sustainability, even if this means tolerating inflation above target.

The third force is the slow erosion of the unipolar currency system. De-dollarisation is progressing at a moderate but cumulative pace, driven by the diversification of central bank foreign exchange reserves, the multiplication of local currency settlement agreements and the coordinated efforts of certain emerging economies to reduce their dependence on the dollar. Gold, in this context, has regained its role as a reserve asset, as reflected in the sustained net purchases by central banks over recent years. Convergent signals further suggest that silver could gradually benefit from a similar logic, fed by both industrial demand and strategic stockpiling behaviour.

Gold and silver: the return of monetary assets

In this context, gold and silver occupy a distinctive position that warrants separate treatment. Gold is no longer merely an occasional safe-haven asset or an inflation hedge: it is gradually reclaiming its role as a reserve asset, as reflected in the convergent behaviour of numerous central banks over several years. Cumulative net purchases now significantly exceed levels observed in previous decades, and reflect an active search for alternatives to the concentration of reserves in sovereign bonds denominated in reference currencies. This movement, structural rather than cyclical, profoundly alters the supply-demand dynamics of the gold market, where mining production is rising slowly while official purchases continue to rise.

Silver presents a distinct but complementary profile. Added to the historical monetary heritage it shares with gold is a considerable industrial dimension, driven by demand from photovoltaics, power electronics and electrical and electronic applications. This dual nature, monetary and industrial, places it at the intersection of the two major themes developed in this document: the re-rating of real assets in the face of monetary expansion, and the growing demand pressure on strategic metals supply chains. Several indicators suggest that a gradual rebuilding of strategic stockpiles, combined with a structural supply deficit, is creating a tight environment that may prove durable.

For the wealth investor, gold and silver thus play complementary roles: gold as a long-term monetary anchor within a wealth-preservation framework, silver as an asset more exposed to both monetary dynamics and electrification themes. Both fit within the same fundamental logic, that of assets whose supply remains structurally inelastic in the short and medium term.

Relative valuation that remains attractive

Beyond macroeconomic arguments, the question of valuation deserves attention. The listed mining sector currently represents only around 0.4% of global market capitalisation, a historically low ratio that reflects a long period of institutional investor disaffection. This structural underrepresentation contrasts with the sector’s new strategic centrality.

Valuation multiples reflect this anomaly. Diversified mining companies trade at EV/EBITDA multiples generally between 6 and 8 times, compared with multiples of 13 to 22 times for the major market sectors (technology, healthcare, consumer goods). This gap is all the more notable given that the operating margins of top-tier producers have improved markedly, on the back of capital allocation discipline, rigorous cost management and a more favourable price environment.

Free cash flow generation has also strengthened, creating the conditions for a shareholder return policy supported by dividends and share buybacks. The expected trajectory of free cash flow generation over the coming years, against a backdrop of sustained prices and controlled investment, constitutes a fundamental support for the sector’s performance.

Production costs and the need for a selective approach

Exposure to the mining sector also requires close attention to cost structures. Producers remain sensitive to changes in energy prices, certain chemical inputs and logistics. As an indication, a USD 10 increase in the oil price may translate into a meaningful rise in operating costs, both for gold producers and for copper producers.

This reality reinforces the importance of a selective approach, attentive to asset quality, jurisdiction of operation, cost structure and operator financial strength. Producers with vertical integration, geographic diversification and access to competitive energy sources retain a marked relative advantage in this environment.

An undervalued strategic asymmetry

Beyond valuation and fundamentals, the sector offers an asymmetric profile that few other asset classes provide. In a scenario of heightened geopolitical tensions, trade fragmentation, persistent inflation or a confidence crisis affecting certain currencies, mining assets (and more broadly real assets) display hedging properties that are difficult to replicate through traditional equity markets. This asymmetry, still largely absent from conventional institutional allocations, in our view constitutes one of the strongest arguments for a measured and active exposure to the sector within a balanced private wealth allocation.

VI. APIS PERSPECTIVE

At APIS Asset Management, we consider that the analysis of strategic metals today goes beyond a strictly sectoral framework: it forms part of a broader reflection on industrial sovereignty, energy security and the re-rating of real assets within private wealth allocations. Several of our investment strategies naturally align with this perspective.

Our reading of the current cycle rests on a conviction: the dynamic under way does not stem from a passing cyclical rebound, but from a structural re-rating of strategic commodities within the global economic and financial architecture. This conviction leads us to favour a selective approach, founded on the quality of underlying assets, the capital allocation discipline of operators, exposure to the most structurally constrained metals, and particular attention to dimensions of governance, jurisdiction and operational resilience.

Within our strategies dedicated to real assets, this reading has recently translated into a gradual repositioning towards strategic industrial metals and energy assets. Copper producers with top-tier assets, established players in the uranium sector supported by renewed interest in civil nuclear power, and selective exposures to the conventional energy sector appear to us today to offer relevant anchor points within a logic of positive sensitivity to inflationary environments and of exposure to a long-term industrial investment cycle. This adjustment, implemented over the past few months, reflects our conviction that the scarcity premium now tends to shift from precious metals alone towards the full range of resources critical to the value chains of the energy and industrial transition.

Within an overall private wealth allocation, we believe that a measured exposure to critical resources, directly or via listed mining equities, may play several complementary roles: a hedge against structural inflation, diversification against de-dollarisation risks, participation in a long-term industrial investment cycle, and contribution to the re-rating of assets still under-represented in institutional portfolios. This exposure is intended neither to substitute for the traditional pillars of an allocation (high-quality sovereign bonds, diversified listed equities, real estate), nor to dominate the portfolio, but to complement these blocks by adding a dimension of strategically positioned real assets.

The current environment appears to us to warrant renewed attention from wealth investors with a sufficient investment horizon and a tolerance for the sector’s inherent volatility. Analytical discipline, selectivity and in-depth knowledge of sectoral dynamics remain, in our view, the principal determinants of performance in this universe.

VII. CONCLUSION

The return of metals to the centre of the global economy is not a passing phenomenon. It reflects a profound recomposition of strategic hierarchies, in which security of supply, industrial autonomy and mastery of the critical nodes of the value chain now take precedence over considerations of efficiency alone. This paradigm shift comes hand in hand with a macroeconomic environment that provides durable support for real assets, in a world marked by sovereign indebtedness, structural inflation and monetary fragmentation.

For the wealth investor, the conjunction of these dynamics creates a singular framework. The critical resources sector remains under-owned, relatively undervalued, and exposed to structural forces that should play out over several cycles. Selectivity, analytical rigour and patience will be the key factors in benefiting from it.

More broadly, the integration of real assets into sophisticated private wealth allocations has become an essential consideration. In a world where the certainties of the previous economic order have eroded, where inflation has ceased to be a passing anomaly and where geopolitics is now part of price formation, diversification towards strategic resources continues a long tradition: the preservation of real capital across successive generations.

VIII. DISCLAIMER

This document has been prepared by APIS Asset Management for information purposes only. It does not constitute an offer to subscribe, a solicitation to invest, or investment advice, and shall not be construed as such. The analyses, opinions and estimates it contains reflect the judgement of their authors as at the date of publication and are subject to change without notice. Past performance is not indicative of future performance. Investments in precious metals and related financial instruments involve risks, including market, volatility, liquidity and capital loss risks. This document does not take into account the particular financial situation, investment objectives or specific needs of any recipient. It is the reader’s responsibility to conduct their own analysis and, where appropriate, to consult their professional advisers before any investment decision. Reproduction or distribution of this document, in whole or in part, is prohibited without the prior authorisation of APIS Asset Management.

IX. SOURCES

U.S. Geological Survey (USGS)

S&P Global Commodity Insights

Australian Government, Department of Industry, Science and Resources

Public disclosures of listed companies (Lithium Americas, MP Materials, Newmont, Capstone)

Métaux stratégiques : Le retour des actifs réels dans un monde fragmenté

Une réflexion patrimoniale sur la souveraineté industrielle, la sécurité énergétique et la revalorisation des ressources critiques.

Une réflexion patrimoniale sur la souveraineté industrielle, la sécurité énergétique et la revalorisation des ressources critiques.

Pour investisseurs patrimoniaux et professionnels de l’allocation

I. INTRODUCTION STRATÉGIQUE

Le rôle des métaux dans l'économie mondiale est en train de changer de nature. Longtemps considérés comme de simples intrants industriels, dont le prix oscillait au gré des cycles macroéconomiques, ils sont aujourd'hui réinvestis d'une dimension qui les rapproche davantage des actifs stratégiques que des matières premières conventionnelles. Cette mutation n'est pas conjoncturelle. Elle traduit une recomposition profonde des rapports de force économiques, technologiques et géopolitiques, dans un monde devenu structurellement plus fragmenté.

Trois forces convergent pour redessiner ce paysage. D'abord, une demande structurellement plus intense, portée par l'électrification généralisée des économies, le déploiement à grande échelle de l'intelligence artificielle, la transformation des systèmes énergétiques et la modernisation des capacités de défense. Ensuite, une offre contrainte, héritière d'une décennie de sous-investissement chronique et désormais soumise à des goulots d'étranglement géologiques, opérationnels et politiques. Enfin, une économie politique nouvelle, dans laquelle les États redeviennent acteurs directs de la sécurisation des chaînes d'approvisionnement, par le biais de subventions, de prises de participation, de constitution de stocks stratégiques et d'instruments de contrôle à l'exportation.

À cette triple dynamique sectorielle s'ajoute un environnement macroéconomique qui renforce l'attrait des actifs tangibles. Les niveaux d'endettement souverain dans les économies développées, la persistance de pressions inflationnistes, la perspective d'une domination fiscale prolongée et la lente érosion du système monétaire unipolaire constituent un arrière-plan favorable aux actifs réels, qu'il s'agisse des métaux précieux, des métaux industriels ou des actifs miniers cotés.

Pour l'investisseur patrimonial, ces évolutions ouvrent un champ de réflexion qui dépasse l'analyse cyclique habituelle. Il ne s'agit plus seulement d’anticiper un rebond cyclique des matières premières, mais d'intégrer les ressources critiques dans une logique d'allocation stratégique de long terme, articulée autour de la souveraineté industrielle, de la sécurité énergétique et de la préservation du pouvoir d'achat réel.

II. POURQUOI LES MÉTAUX STRATÉGIQUES REDEVIENNENT CENTRAUX

Une demande tirée par les grandes mutations technologiques

Le retour des métaux au cœur de l'économie mondiale s'explique en premier lieu par l'ampleur des besoins générés par les transformations technologiques en cours. L'électrification n'est plus une thématique sectorielle limitée à la mobilité électrique ou aux énergies renouvelables : elle traverse désormais l'ensemble des chaînes industrielles, des infrastructures de transport aux réseaux de distribution, des bâtiments aux centres de données.

L'intelligence artificielle illustre cette dynamique de manière particulièrement frappante. La multiplication des centres de données et des infrastructures de calcul intensif entraîne une croissance accélérée de la demande d'électricité, qu'une part croissante des opérateurs s'efforce d'orienter vers des sources renouvelables ou bas-carbone. Cette demande supplémentaire exige à son tour davantage de cuivre pour le câblage, d'aluminium pour les structures, de nickel et de cobalt pour le stockage, et d'uranium pour la production électrique de base.

Les ordres de grandeur sont significatifs. À l'horizon 2035, la demande de cuivre devrait progresser d'environ 29 %, celle d'aluminium de 23 %, celle d'uranium de 29 %, tandis que la demande de lithium pourrait être multipliée par plus de quatre. En Chine, premier marché industriel mondial, la consommation de cuivre et d'aluminium liée aux technologies propres devrait dépasser dès cette année la demande issue du secteur traditionnel de la construction, marquant un basculement structurel des moteurs de consommation.

Le réarmement comme facteur structurel de demande

À cette dynamique civile s'ajoute un renforcement de la demande liée aux besoins militaires. Les systèmes de défense modernes sont fortement consommateurs de cuivre pour l'électronique, de tungstène pour les munitions, de nickel pour les applications aérospatiales et de terres rares pour les aimants permanents qui équipent les systèmes de guidage avancés. L'asymétrie économique des conflits contemporains (missiles intercepteurs coûteux face à des drones bon marché) pèse également sur les stocks et accentue la pression sur les filières d'approvisionnement.

Les conflits récents au Moyen-Orient ont confirmé cette tendance. Les programmes pluriannuels de réarmement engagés dans la plupart des grandes économies occidentales, ainsi qu'au Japon, en Corée du Sud et en Inde, prolongent ce mouvement de fond. La sécurité des approvisionnements en métaux critiques est désormais traitée, dans nombre de doctrines stratégiques, au même titre que la sécurité énergétique l'avait été dans les décennies passées.

Une offre structurellement contrainte

Face à cette demande, l'appareil productif minier se heurte à des limites de plus en plus tangibles. Les délais de développement des projets se sont allongés : un nouveau gisement de cuivre nécessite aujourd'hui près de dix-huit ans pour atteindre la production, contre une douzaine d'années au milieu des années 2000. Les teneurs minérales déclinent dans la plupart des gisements historiques. Les processus d'autorisation se sont alourdis. Les contraintes environnementales et sociales se sont renforcées. Le coût du capital nécessaire au lancement de nouveaux projets, dans un contexte de taux longs durablement plus élevés, constitue un frein additionnel.

Conséquence logique : des déficits d'offre sont anticipés à l’horizon 2030-2035 pour plusieurs métaux stratégiques, notamment le cuivre, le cobalt, l'uranium et le lithium. Ces déséquilibres devraient soutenir durablement les prix et créer un environnement favorable aux producteurs disposant d'actifs de qualité, d'une discipline d'allocation du capital et d'une exposition aux métaux les plus contraints.

III. LA GÉOPOLITIQUE DES CHAÎNES D'APPROVISIONNEMENT

Concentration géographique et asymétrie des dépendances

L'une des caractéristiques les plus saisissantes du paysage actuel tient à la concentration géographique extrême des chaînes d'approvisionnement en métaux critiques. Les opérations minières comme les capacités de raffinage et de transformation sont concentrées dans un nombre restreint de juridictions, souvent en dehors de l'OCDE, ce qui crée des dépendances asymétriques pour les économies occidentales.

La Chine occupe une position dominante sur l'ensemble de la chaîne de valeur. Elle représente une part majoritaire du raffinage mondial de terres rares, contrôle une fraction substantielle de la transformation du lithium, du graphite, du tungstène, et joue un rôle central dans le traitement du cuivre, du nickel et de l'aluminium. Cette domination ne résulte pas seulement d'avantages géologiques, mais d'un effort stratégique étalé sur plusieurs décennies, combinant investissements industriels, politique énergétique et intégration verticale.

D'autres acteurs occupent des positions critiques sur des segments spécifiques. L'Indonésie domine désormais la filière du nickel, avec une part majoritaire de la production mondiale et une capacité de transformation en forte croissance. La République démocratique du Congo concentre une part déterminante de l'offre de cobalt. L'Australie reste un pourvoyeur essentiel de lithium et de bauxite. Le Kazakhstan, le Canada et le Niger jouent un rôle clé dans le cycle de l'uranium. Cette répartition crée une carte des dépendances qui ne recoupe pas nécessairement les alliances diplomatiques traditionnelles.

Vulnérabilité des routes commerciales

À cette concentration de la production s'ajoute la fragilité des routes maritimes par lesquelles transitent ces flux. Les détroits stratégiques (Ormuz, Malacca, Bab el-Mandeb, Suez) constituent autant de points de passage critiques dont la perturbation peut affecter significativement les approvisionnements. Le conflit au Moyen-Orient a rappelé que les risques pesant sur ces corridors logistiques ne sont pas théoriques : ils se traduisent par des hausses de coûts d'assurance maritime, des allongements de délais et, dans certains cas, par des arrêts de production.

L'exemple de l'aluminium est instructif. Le Golfe persique concentre environ 9 % de la capacité mondiale de production primaire, dont l'essentiel transite par le détroit d'Ormuz. Toute perturbation prolongée de cette voie peut placer plusieurs millions de tonnes de production en situation de risque, avec des conséquences immédiates sur les prix internationaux et sur la stabilité des chaînes d'approvisionnement aval.

Les contrôles à l'exportation comme arme stratégique

L'arsenal des politiques commerciales a également évolué. Les contrôles à l'exportation, jadis marginaux dans le secteur minier, sont devenus un instrument central. La Chine en a fait un usage croissant ces dernières années, en restreignant successivement les exportations de gallium, de germanium, d'antimoine, de graphite, puis d'équipements de transformation. Des signaux indiquent que des restrictions pourraient s'étendre aux technologies de raffinage des terres rares elles-mêmes, ce qui constituerait un saut qualitatif majeur dans l'instrumentalisation des chaînes critiques.

Ces décisions s'inscrivent dans la continuité d'épisodes historiques. Les restrictions chinoises sur les terres rares au cours de la dernière décennie avaient déjà perturbé les marchés mondiaux et conduit plusieurs économies (États-Unis, Japon, Australie en particulier) à engager des stratégies de diversification. La répétition de ces épisodes, dans un contexte de rivalité technologique accrue, alimente la prise de conscience de la vulnérabilité structurelle des économies occidentales.

IV. LE RETOUR DE L'ÉTAT STRATÈGE

Les États-Unis : d'une politique de financement à une politique d'actionnariat

Face à ces dépendances, les économies occidentales redéploient leur arsenal de politique industrielle avec une intensité inédite depuis plusieurs décennies. Les États-Unis ont ouvert la voie. L'Inflation Reduction Act de 2022 avait posé les premières bases d'un soutien massif aux chaînes de valeur stratégiques, en combinant crédits d'impôt à la production, exigences de contenu domestique et incitations à la relocalisation. Si certaines dispositions ont été ajustées lors des changements politiques ultérieurs, l'architecture générale du dispositif est demeurée structurante.

L'étape suivante a été franchie avec le One Big Beautiful Bill Act, qui consacre pour la première fois une enveloppe explicitement dédiée à l'extraction, au raffinage et à la transformation des minéraux critiques. Le dispositif prévoit jusqu'à 5 milliards de dollars d'investissement direct, 500 millions de dollars de subventions de crédit susceptibles de mobiliser jusqu'à 100 milliards de dollars en garanties de prêts, et 3,3 milliards de dollars pour des contrats d'achat de long terme. À ce dispositif s'ajoute Project Vault, qui vise à constituer une réserve stratégique nationale de 12 milliards de dollars couvrant les terres rares, le lithium et le nickel.

Au-delà des nouvelles lois, des cadres existants ont été réorientés. Le Defense Production Act, la Export-Import Bank, la Development Finance Corporation et même certains volets du CHIPS Act sont aujourd'hui mobilisés pour soutenir des projets miniers, en territoire national comme à l'international. L'estimation cumulée des engagements de l'administration américaine actuelle approche les 18,6 milliards de dollars, répartis sur une soixantaine de projets.

Le changement le plus notable réside dans la nature de ces interventions. Washington ne se contente plus de prêter ou de subventionner : l'État américain entre désormais directement au capital de certaines entreprises minières. Le projet Thacker Pass de Lithium Americas, initialement soutenu par un prêt du Département de l'Énergie, a évolué vers une participation directe en fonds propres, couplée à une coentreprise avec General Motors. MP Materials, opérateur de la seule mine active de terres rares aux États-Unis, a fait l'objet d'un investissement stratégique de 550 millions de dollars de la part du Département de la Défense. Ce passage d'une logique de financement à une logique d'actionnariat constitue une rupture historique avec la doctrine de non-intervention qui prévalait jusqu'alors.

Une mobilisation occidentale élargie

Ce mouvement déborde largement le cadre américain. L'initiative Pax Silica, conduite sous l'égide des États-Unis, vise à structurer une chaîne d'approvisionnement occidentale en métaux critiques liés à l'intelligence artificielle, d'une valeur estimée à 1 000 milliards de dollars. Le partenariat critique minéraux signé entre les États-Unis et l'Australie en 2025 mobilise 8,5 milliards de dollars de financements de projets, en réponse directe à la prééminence chinoise.

L'Union européenne avance dans une logique complémentaire, articulée autour du Critical Raw Materials Act et de l'initiative RESourceEU, dont l'ambition est de créer un centre européen de monitoring, d'achat groupé et de stockage de matières premières critiques. La France, l'Allemagne et l'Italie animent une coordination renforcée. Le Royaume-Uni explore des dispositifs de stockage stratégique via l'OTAN et des cadres nationaux dédiés.

En Asie, le Japon et la Corée du Sud disposent déjà de systèmes de réserves gérés par les autorités publiques et continuent à étendre leur réseau de partenariats internationaux. L'Inde a lancé sa National Critical Mineral Mission, tandis que des accords bilatéraux entre le Japon et l'Australie viennent compléter le maillage.

Une nouvelle économie politique des ressources

Ce que dessinent ces évolutions, prises ensemble, est un changement de paradigme. Pendant plusieurs décennies, la doctrine dominante reposait sur l'efficience des marchés mondiaux, la spécialisation internationale et l'optimisation des coûts. Le pendule s'est déplacé : la résilience, la sécurité d'approvisionnement et le contrôle des nœuds stratégiques de la chaîne de valeur priment désormais sur l'optimisation pure. Les implications pour les marchés sont substantielles, car cette nouvelle économie politique introduit une prime de risque géopolitique durable dans la formation des prix, et un soutien structurel à la valorisation des actifs stratégiquement situés.

V. PERSPECTIVE D'INVESTISSEMENT PATRIMONIALE

Le retour des actifs réels dans les allocations

Pour l'investisseur patrimonial, le contexte décrit appelle une réflexion qui dépasse la lecture cyclique habituelle. Plusieurs forces convergent pour replacer les actifs réels au centre des allocations stratégiques de long terme.

La première tient à l'environnement inflationniste. La masse monétaire américaine M2 a progressé d'environ 48 % depuis le début de 2020, ce qui signifie qu'environ un tiers des dollars actuellement en circulation ont été créés sur une période très courte. À cette expansion monétaire s'ajoutent les effets inflationnistes des politiques tarifaires, des tensions sur les chaînes d'approvisionnement et des crises énergétiques liées aux conflits récents. Dans un tel environnement, les actifs dont l'offre est par nature contrainte (métaux précieux, métaux industriels critiques, ressources foncières) conservent un avantage relatif notable face aux actifs purement financiers.

La deuxième concerne les niveaux d'endettement souverain. Le ratio dette publique sur PIB aux États-Unis approche 122 %, contre 32 % à la fin des années 1970. Les coûts de service de la dette fédérale dépassent désormais 1 000 milliards de dollars par an, soit environ 19 % des recettes fédérales, et excèdent le budget de la défense. Cette configuration crée une contrainte structurelle sur la marge de manœuvre des banques centrales et accroît la probabilité d'une domination fiscale prolongée, dans laquelle la politique monétaire reste accommodante pour soutenir la soutenabilité budgétaire, quitte à tolérer une inflation supérieure aux cibles.

La troisième force est la lente érosion du système monétaire unipolaire. La dé-dollarisation progresse, à un rythme modéré mais cumulatif, sous l'effet de la diversification des réserves de change des banques centrales, de la multiplication des accords de règlement en devises locales et des efforts coordonnés de certains pays émergents pour réduire leur dépendance au dollar. L'or, dans ce contexte, a regagné son rôle d'actif de réserve, comme en témoignent les achats nets soutenus des banques centrales depuis plusieurs années. Des signaux convergents suggèrent par ailleurs que l'argent métal pourrait progressivement bénéficier d'une logique similaire, alimentée à la fois par la demande industrielle et par des comportements de constitution de stocks stratégiques.

Or et argent : le retour des actifs monétaires

Dans ce contexte, l'or et l'argent occupent une place singulière qui mérite d'être traitée pour elle-même. L'or n'est plus simplement un actif refuge ponctuel ou une couverture contre l'inflation : il retrouve progressivement son rôle d'actif de réserve, comme en témoignent les comportements convergents de nombreuses banques centrales depuis plusieurs années. Les achats nets cumulés dépassent désormais largement les niveaux observés au cours des décennies précédentes, et traduisent une recherche active d'alternatives à la concentration des réserves en obligations souveraines libellées en devises de référence. Ce mouvement, structurel plutôt que cyclique, modifie en profondeur la dynamique de l'offre et de la demande sur le marché aurifère, où la production minière progresse lentement face à des achats officiels qui s'inscrivent dans la durée.

L'argent métal présente un profil distinct mais complémentaire. À l’héritage monétaire historique qu’il partage avec l’or s'ajoute une dimension industrielle considérable, alimentée par la demande du photovoltaïque, de l'électronique de puissance et des applications électriques et électroniques. Cette double nature, monétaire et industrielle, le place à l'intersection des deux grandes thématiques développées dans ce document : la revalorisation des actifs réels face à l'expansion monétaire, et la pression croissante de la demande sur les chaînes d'approvisionnement en métaux stratégiques. Certains signaux suggèrent qu'une reconstitution progressive des stocks stratégiques, conjuguée à un déficit structurel d'offre, crée un environnement de tension qui pourrait s'avérer durable.

Pour l'investisseur patrimonial, l'or et l'argent jouent ainsi des rôles complémentaires : l'or comme ancrage monétaire de long terme dans une logique de préservation, l'argent comme actif davantage exposé à la fois aux dynamiques monétaires et aux thématiques d'électrification. L'un comme l'autre s'inscrivent dans la même logique fondamentale, celle d'actifs dont l’offre demeure structurellement peu élastique à court et moyen terme.

Une valorisation relative qui demeure attractive

Au-delà des arguments macroéconomiques, la question de la valorisation mérite attention. Le secteur minier coté ne représente actuellement qu'environ 0,4 % de la capitalisation boursière mondiale, ratio historiquement bas qui traduit une longue période de désaffection des investisseurs institutionnels. Cette sous-représentation structurelle contraste avec la centralité stratégique nouvelle du secteur.

Les multiples de valorisation reflètent cette anomalie. Les sociétés minières diversifiées se traitent à des EV/EBITDA généralement compris entre 6 et 8 fois, à comparer à des multiples de 13 à 22 fois pour les grands secteurs de marché (technologie, santé, biens de consommation). Cet écart est d'autant plus notable que les marges opérationnelles des producteurs de premier rang se sont nettement améliorées, sous l'effet d'une discipline d'allocation du capital, d'une gestion rigoureuse des coûts et d'un environnement de prix plus favorable.

La génération de trésorerie disponible s'est également renforcée, créant les conditions d'une politique de retour aux actionnaires soutenue par des dividendes et des rachats d'actions. La trajectoire attendue de cette génération de trésorerie sur les prochaines années, dans un contexte de prix soutenus et d'investissements maîtrisés, constitue un point d'appui fondamental pour la performance du secteur.

Coûts de production et nécessité d’une approche sélective

Une exposition au secteur minier suppose également une lecture attentive des structures de coûts. Les producteurs demeurent sensibles à l’évolution des prix de l’énergie, de certains intrants chimiques et de la logistique. À titre indicatif, une hausse de USD 10 du prix du baril peut se traduire par une augmentation sensible des coûts opérationnels, tant pour les producteurs d’or que pour ceux de cuivre.

Cette réalité renforce l’importance d’une approche sélective, attentive à la qualité des actifs, à la juridiction d’opération, à la structure des coûts et à la solidité financière des opérateurs. Les producteurs disposant d’une intégration verticale, d’une diversification géographique et d’un accès à des sources énergétiques compétitives conservent un avantage relatif marqué dans cet environnement.

Une asymétrie stratégique sous-évaluée

Au-delà de la valorisation et des fondamentaux, le secteur offre un profil asymétrique que peu d'autres classes d'actifs procurent. Dans un scénario de tensions géopolitiques accrues, de fragmentation commerciale, d'inflation persistante ou de crise de confiance dans certaines devises, les actifs miniers (et plus largement les actifs réels) présentent des propriétés de couverture difficilement reproductibles par les marchés actions traditionnels. Cette asymétrie, encore largement absente des allocations institutionnelles classiques, constitue à notre sens l'un des arguments les plus forts en faveur d'une exposition mesurée et active au secteur dans une allocation patrimoniale équilibrée.

VI. PERSPECTIVE APIS

Chez APIS Asset Management, nous considérons que l'analyse des métaux stratégiques dépasse aujourd'hui le simple cadre sectoriel : elle s'inscrit dans une réflexion plus large sur la souveraineté industrielle, la sécurité énergétique et la revalorisation des actifs réels dans les allocations patrimoniales. Certaines de nos stratégies d'investissement s'inscrivent naturellement dans cette réflexion.

Notre lecture du cycle actuel repose sur une conviction : la dynamique en cours ne relève pas d’un rebond cyclique passager, mais d’une revalorisation structurelle des matières premières stratégiques dans l’architecture économique et financière mondiale. Cette conviction nous conduit à privilégier une approche sélective, fondée sur la qualité des actifs sous-jacents, la discipline d’allocation du capital des opérateurs, l’exposition aux métaux les plus structurellement contraints, ainsi qu’une attention particulière aux dimensions de gouvernance, de juridiction et de résilience opérationnelle.

Au sein de nos stratégies dédiées aux actifs réels, cette lecture s’est traduite récemment par un repositionnement progressif vers les métaux industriels stratégiques et les actifs énergétiques. Les producteurs de cuivre disposant d’actifs de premier rang, les acteurs établis du secteur de l’uranium portés par le regain d’intérêt pour le nucléaire civil, ainsi que des expositions sélectives au secteur énergétique conventionnel nous paraissent constituer aujourd’hui des points d’appui pertinents dans une logique de sensibilité favorable aux régimes inflationnistes et de capture du cycle d’investissement industriel. Cette inflexion, opérée au cours des derniers mois, traduit notre conviction que la prime de rareté tend désormais à se déplacer des seuls métaux précieux vers l’ensemble des ressources critiques pour les chaînes de valeur de la transition énergétique et industrielle.

Dans le cadre d'une allocation patrimoniale globale, nous estimons qu'une exposition mesurée aux ressources critiques, directe ou via les sociétés minières cotées, peut jouer plusieurs rôles complémentaires : couverture contre l'inflation structurelle, diversification face aux risques de dé-dollarisation, capture d'un cycle d'investissement industriel de long terme, et participation à la revalorisation d'actifs encore sous-représentés dans les portefeuilles institutionnels. Cette exposition n'a vocation ni à se substituer aux piliers traditionnels d'une allocation (obligations souveraines de qualité, actions cotées diversifiées, immobilier), ni à dominer le portefeuille, mais à compléter ces blocs en y apportant une dimension d'actifs réels stratégiquement positionnés.

L'environnement actuel nous semble justifier une attention renouvelée de la part des investisseurs patrimoniaux disposant d'un horizon d'investissement suffisant et d'une tolérance à la volatilité propre au secteur. La discipline d'analyse, la sélectivité et la connaissance approfondie des dynamiques sectorielles restent, à notre sens, les déterminants principaux de la performance dans cet univers.

VII. CONCLUSION

Le retour des métaux au centre de l'économie mondiale n'est pas un épiphénomène. Il traduit une recomposition profonde des hiérarchies stratégiques, dans laquelle la sécurité d'approvisionnement, l'autonomie industrielle et la maîtrise des nœuds critiques de la chaîne de valeur priment désormais sur les seules considérations d'efficience. Ce changement de paradigme s'accompagne d'un environnement macroéconomique qui soutient durablement les actifs réels, dans un monde marqué par l'endettement souverain, l'inflation structurelle et la fragmentation monétaire.

Pour l'investisseur patrimonial, la conjonction de ces dynamiques crée un cadre singulier. Le secteur des ressources critiques demeure sous-détenu, sous-valorisé en termes relatifs, et exposé à des forces structurelles qui devraient déployer leurs effets sur plusieurs cycles. La sélectivité, la rigueur analytique et la patience constitueront les facteurs clés pour en tirer parti.

Plus largement, l'intégration des actifs réels dans les allocations patrimoniales sophistiquées s'impose aujourd'hui comme une réflexion incontournable. Dans un monde où les certitudes du précédent ordre économique se sont effritées, où l'inflation a cessé d'être une anomalie passagère et où la géopolitique s'invite désormais dans la formation des prix, la diversification vers les ressources stratégiques s'inscrit dans la continuité d'une tradition longue : celle de la préservation, par les générations qui se succèdent, du capital réel.

VIII. AVERTISSEMENT

Le présent document a été préparé par APIS Asset Management à des fins exclusivement informatives. Il ne constitue ni une offre de souscription, ni une sollicitation d'investissement, ni un conseil en investissement, et ne saurait être interprété comme tel. Les analyses, opinions et estimations qu'il contient reflètent le jugement de leurs auteurs à la date de publication et sont susceptibles d'évoluer sans préavis. Les performances passées ne préjugent pas des performances futures. Tout investissement comporte des risques, y compris un risque de perte en capital, et doit être apprécié au regard de la situation patrimoniale, des objectifs et de l'horizon d'investissement propres à chaque investisseur. Il appartient au lecteur de procéder à sa propre analyse et, le cas échéant, de consulter ses conseillers professionnels avant toute décision d'investissement. La reproduction ou la diffusion du présent document, en tout ou en partie, est interdite sans autorisation préalable d'APIS Asset Management.

IX. SOURCES

U.S. Geological Survey (USGS)

S&P Global Commodity Insights

Australian Government, Department of Industry, Science and Resources

Documents publics des sociétés cotées (Lithium Americas, MP Materials, Newmont, Capstone)

Market Update – Precious Metals and Mining Equities

The gold sector has experienced a notable correction over the past week, which may raise questions regarding its safe haven role, particularly in the context of ongoing geopolitical tensions in the Middle East. While market conditions remain uncertain, we believe this recent dislocation offers an attractive entry point for disciplined investors looking to build or reinforce exposure to the sector.

The gold sector has experienced a notable correction over the past week, which may raise questions regarding its safe haven role, particularly in the context of ongoing geopolitical tensions in the Middle East. While market conditions remain uncertain, we believe this recent dislocation offers an attractive entry point for disciplined investors looking to build or reinforce exposure to the sector.

In response to the recent sell-off, the Apis Asset Management team has acted swiftly to reposition both our Precious Metals and Electrum strategies, with a view to navigating near-term volatility while preparing for the recovery we expect as underlying fundamentals reassert themselves.

In our view, the recent pullback in gold has been primarily driven by short-term macroeconomic factors and liquidity pressures, rather than any deterioration in the long-term investment case. A sharp rise in US real yields, combined with a stronger US dollar, has weighed on gold, silver and mining equities. This movement, which has brought gold prices back to levels last seen in December, has likely been amplified by profit-taking following the sector’s strong performance in early 2026. Gold mining equities have similarly retraced.

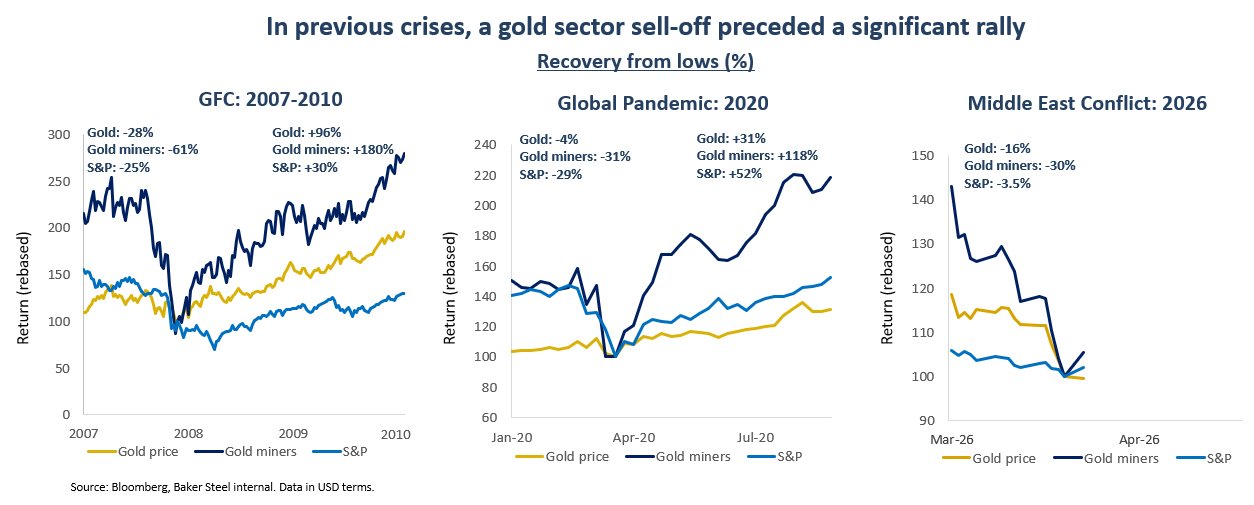

Such corrections are not uncommon within broader bull markets. History offers several relevant precedents. During the Global Financial Crisis in 2008, as well as during the market stress of the 2020 pandemic, gold and precious metals miners experienced significant drawdowns before entering strong recovery phases. In both instances, mining equities led the rebound, outperforming both physical gold and broader equity markets.

In previous periods of market stress, gold and gold mining equities experienced short-term drawdowns before entering strong recovery phases.

We believe the current environment presents a comparable setup, as the fundamental backdrop for the sector remains intact. While short-term volatility may persist, particularly if broader equity markets weaken, current geopolitical developments are increasing the risks of inflation, stagflation and widening fiscal deficits. The growing burden of US federal debt, combined with political pressure to maintain accommodative monetary conditions, points towards a regime of financial repression, especially if real rates turn negative. In such an environment, gold and precious metals continue to play a key role as stores of value.

At the same time, central bank demand remains supportive, while structural demand for metals such as silver (particularly linked to solar photovoltaics) continues to strengthen. Combined with constrained physical supply, these factors underpin a robust long-term outlook for the sector.

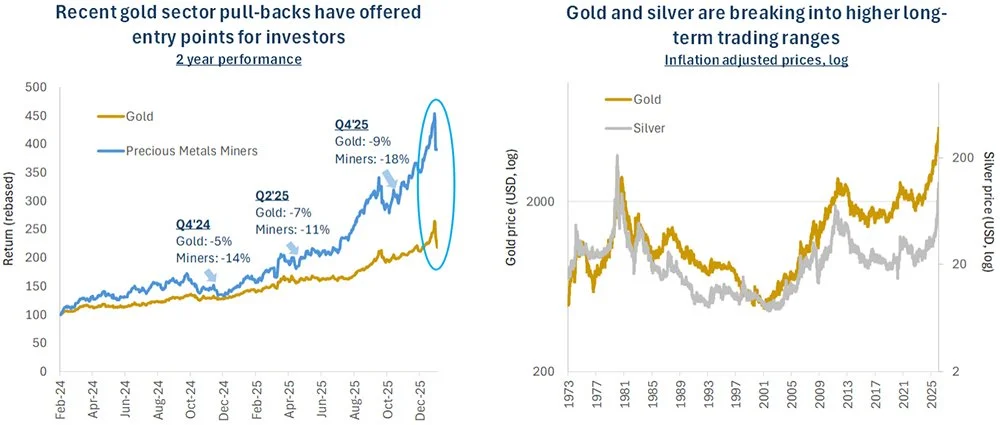

Against this backdrop, we have used recent market weakness to selectively increase exposure to high-quality, undervalued mid-cap gold miners, while carefully reassessing risk profiles across the portfolio. We have also rotated towards companies less exposed to potential energy supply disruptions and are actively engaging with management teams to assess their ability to manage rising production costs and potential supply chain pressures.

We remain confident in the outlook for gold and precious metals equities and believe current conditions are laying the foundations for the next phase of the cycle. Despite potential cost pressures, the sector continues to benefit from strong margins and disciplined capital allocation. More broadly, we also see emerging opportunities across industrial and speciality metals impacted by the current environment.

With mining equities trading at attractive valuations, both on a historical and relative basis, we continue to identify opportunities through a disciplined and selective investment approach.

Thank you for your continued trust. Should you wish to discuss recent market developments or portfolio positioning in more detail, we remain at your disposal.

We remain at your disposal for any further information.

Kind regards,

Apis Asset Management

Market Update – Precious Metals and Mining Equities

Recent market movements have led to a corrective phase in both gold and silver prices after the strong rally that took place in January, when gold traded above USD 5,400 per ounce and silver exceeded USD 116 per ounce. Mining equities have followed this pullback, declining alongside the underlying metals.

Recent market movements have led to a corrective phase in both gold and silver prices after the strong rally that took place in January, when gold traded above USD 5,400 per ounce and silver exceeded USD 116 per ounce. Mining equities have followed this pullback, declining alongside the underlying metals.

From a long-term investment perspective, such periods of consolidation have historically offered constructive entry points within the precious metals cycle. Corrections of this nature often help rebalance market positioning and bring valuations back to more attractive levels ahead of the next upward phase.

The recent weakness appears to have been driven primarily by profit-taking. Subsequent market commentary pointed to the likely nomination of Kevin Warsh as the next Chair of the US Federal Reserve as a potential explanation for the correction. In our view, this narrative reflects a short-term market interpretation rather than a genuine change in underlying fundamentals.

Regardless of the individual appointed, structural constraints linked to elevated US deficits, rising interest payment burdens, and long-term fiscal imbalances are unlikely to be materially altered. As a result, the broader environment of negative real rates and currency debasement pressures remains intact, a backdrop that continues to support the long-term case for precious metals.

Our positive long-term outlook for the precious metals sector remains intact, as the structural drivers underpinning the bull market in gold and silver remain firmly in place. Continued geopolitical uncertainty and macroeconomic volatility reinforce gold’s role as a strategic reserve asset, particularly for central banks. At the same time, persistent inflationary pressures and the structural challenges associated with elevated levels of US federal debt point toward a prolonged environment of financial repression. Historically, such conditions have supported investment demand for precious metals as a means of preserving purchasing power. In parallel, industrial demand dynamics are also favourable, notably the growing use of silver in photovoltaic solar technologies, while supply conditions for both gold and silver remain constrained.

Looking back over the past two years, similar pullbacks in gold, silver and mining equities have repeatedly proved to be healthy pauses within a broader upward trend. These corrections have typically been shorter and less severe than many market participants anticipated, with prices recovering as underlying fundamentals reasserted themselves. During the previous trough in gold prices in October 2025, the market took just 19 days to reach its low. A sharper correction in the current episode could, therefore, be consistent with a faster subsequent recovery.

In this context, Apis Asset Management is using the current market weakness to position portfolios for the next phase of the metals and mining cycle. We continue to see attractive opportunities across the precious metals mining sector, where companies are benefiting from improved margins, disciplined capital allocation and tighter cost control, leading to stronger profitability. Beyond precious metals, we are also identifying value in other segments of the metals universe that may have been indiscriminately affected by the broader market sell-off.

With mining equities appearing attractively valued, both in historical terms and relative to underlying metal prices, our approach remains focused on selective, active stock picking. This disciplined process is designed to navigate periods of volatility while capturing long-term upside potential as the fundamental backdrop continues to improve.

We remain at your disposal for any further information.

Kind regards,

Apis Asset Management

Patience and Discipline: The Forgotten Virtues of Wealth Management

In a world driven by immediacy and short-term signals, patience and discipline are increasingly undervalued — yet they remain the true foundations of long-term wealth preservation.

At APIS Asset Management, we believe that time, when combined with a coherent strategy and rational discipline, is not a risk but an ally. Precious metals, particularly gold, continue to demonstrate why endurance matters more than speed in resilient portfolio construction.

Investing is not about reacting faster. It is about staying consistent longer.

In an environment dominated by immediacy and volatility, patience and discipline remain the forgotten pillars of successful wealth management. APIS Asset Management embodies these essential virtues as precious metals regain their central role in resilient, long-term portfolios.

Time as an Ally to Performance

Daily market fluctuations frequently encourage reactivity rather than consistency. Yet history shows that the most successful investors share two common traits: patience and discipline.

A Coherent, Long-Term Approach

Wealth management is not a race for speed but a commitment to coherence — understanding market cycles and maintaining direction despite short-term fluctuations. In this perspective, time becomes an ally rather than an adversary.

Gold as a Symbol of Stability

Gold and other precious metals illustrate this philosophy perfectly. Often perceived as defensive or static assets, they have consistently preserved purchasing power and stabilized portfolio performance through multiple market cycles. Their strength lies not in immediacy, but in endurance.

Practicing “Rational Patience”

At APIS Asset Management, we advocate rational patience: accepting temporary volatility to capture the benefits of long-term valuation cycles. This discipline reflects our enduring commitment to stewardship and intergenerational continuity — the very essence of wealth preservation.

A Strategy, Not Inertia

Investing is not a sprint; it is a measured walk. And in that walk, patience is not inertia — it is strategy.

Gold Miners: Structural Discount or Historical Opportunity?

While gold continues to trade near record highs, a striking paradox persists: gold mining companies remain significantly undervalued.

Why does this structural disconnect endure? Is it a risk ... or an opportunity?

At APIS Asset Management, we take a deeper look at this phenomenon and highlight the forces reshaping the sector: renewed financial discipline, ongoing consolidation, stronger balance sheets, and resilient cash flows.

Introduction

While gold prices are trading near record highs, gold mining companies remain paradoxically undervalued. APIS Asset Management analyses the reasons behind this persistent discount and the opportunities it offers to long-term investors within a diversified wealth management allocation.

A Persistent Paradox

As gold reaches new highs, one question remains: why are gold miners still trading at such depressed valuations? Despite strengthened balance sheets, restored profitability, and disciplined capital allocation, the market continues to treat the sector with caution.

A Transformed Industry

Since the previous peak in 2011-2012, the industry has undergone a profound transformation.

Producers have reduced leverage, streamlined costs, and implemented strict shareholder-return policies. Yet valuation multiples — notably the Gold Miners Index vs Gold Spot ratio — remain 40-60% below their long-term average.

Perception Misaligned with Fundamentals

This discount seems driven more by perception than by fundamentals. The memory of past excesses and volatility has left investors wary, even though today’s miners generate robust cash flows and maintain solid margins, even at gold prices below current levels.

Consolidation and Financial Discipline as Catalysts

The ongoing consolidation within the sector serves as another powerful catalyst. Mergers and acquisitions are fostering efficiency, expanding resource bases, and meeting heightened sustainability requirements. Over the medium term, these dynamics should contribute to a rerating in valuations.

An Opportunity for Patient Investors

At APIS Asset Management, we view this discount as a compelling long-term opportunity for investors willing to accept short-term volatility in exchange for significant catch-up potential.

Within a wealth management framework, gold miners remain a tangible, real asset whose value stems from scarcity, operational discipline, and financial resilience.

APIS x Le Figaro

Watch our interview with Le Figaro, where we discuss Apis AM’s vision, values, and commitment to innovation in asset management.

We are proud to share our recent feature in Le Figaro, highlighting Apis AM’s unique approach to asset management.

Gold: a growth opportunity in this dynamic and inflationary environment

Earlier this year, we anticipated that mounting geopolitical tensions, central bank gold accumulation, and market volatility would drive gold prices higher, with positive implications for gold mining stocks. With gold recently reaching a new high of $2,758 per ounce, our expectations have largely been validated, confirming the robust trend in the gold market and creating a favorable environment for mining stocks, which have started closing their long-standing valuation gap with gold itself.

The recent surge in gold prices strengthens the case for undervalued mining stocks, which continue to show profitability improvements as they catch up to gold’s higher prices. This trend points to sustained growth potential, especially as investor interest in mining equities grows alongside expectations of increasing M&A activity in the sector. Despite recent rallies, mining stocks on average remain 60% below their historical peaks, suggesting ample upside potential as the sector gains more traction with institutional investors.

Some high-beta mining stocks are showing promising growth due to their price sensitivity to gold’s movements, offering opportunities for enhanced returns. Companies like Newmont Corporation and Barrick Gold have shown resilience, and mid-tier mining stocks with historical beta could be excellent candidates to capture additional upside. Furthermore, silver mining stocks such as Pan American Silver, Fresnillo, and First Majestic Silver—recently added to our portfolio—offer compelling growth potential as silver prices often follow gold with greater volatility.

While the outlook remains positive, operational and regulatory challenges in the mining sector are worth noting. Rising exploration and operating costs, along with heightened regulatory constraints, have limited immediate valuation gains and are expected to continue presenting headwinds. Additionally, resource nationalization risks in regions such as in South Amarica and Africa, introduce geopolitical risks that require active management. While these risks should be closely monitored, they also reinforce the investment case for gold and silver as safe-haven assets.

At APIS AM, we recognize this environment as an opportunity to leverage our expertise in gold and silver mining equities. With continued geopolitical tensions, central bank buying activity, and favorable fundamentals for gold mining stocks, we see significant upside for well-positioned mining equities.

While the initial market reaction to Trump’s re-election was extremely positive with a huge decrease of the volatility, and a positive trend on the market, we anticipate that inflationary pressures from his policies will support the longer-term case for gold. The Federal Reserve, as expected, lowered its interest rates by 25 basis points on Thursday, November 7, as part of its ongoing strategy to support the economy amid global uncertainties and to extend the current U.S. economic expansion.

However, in light of Trump’s economic policies, this rate-cutting trend could be reconsidered. While Trump has consistently advocated for low interest rates to boost economic growth, some of his policies—such as increased infrastructure spending and protectionist trade measures—could create inflationary pressures over time.

Thus, while the Fed is currently following an accommodative stance, Trump’s policies could shift this dynamic, prompting a more restrictive monetary policy in response to rising inflationary pressures. Trump administration's economic agenda, with a focus on spending, deregulation, and protectionist policies, is likely to drive inflation, weakening potentially the dollar and further boosting demand for gold as a hedge.

In conclusion, the Trump effect—while likely to induce short-term fluctuations—will ultimately amplify the appeal of precious metals as safe-haven assets, potentially benefiting gold and silver mining stocks. With the sustained upward trend in gold prices and narrowing valuation gaps in mining equities, we see compelling growth opportunities for investors who can navigate this dynamic and inflationary environment.

Gold: The new diamond of mining stocks

APIS Asset Management sees a bright outlook for the gold market with resurgence in its value and a positive impact on mining stocks.

APIS Asset Management sees a bright outlook for the gold market with resurgence in its value and a positive impact on mining stocks.

The renewed appeal of gold

In recent months, gold has regained some of its 'shine' to flirt with historic highs. Whilst gold is no longer an exchange currency nor the historical ‘Standard’ set by the US Federal Reserve, and since the Bretton Woods system has long been abandoned, some countries have begun to increase their reserves again. In today’s particular geopolitical, economic, and financial environment, non-aligned countries are increasingly detaching themselves from, if not outright showing defiance towards, the US dollar. More generally, gold acts as a security measure and a hedge against global economic volatility, providing strong backing for emerging currencies and a natural hedge against inflation.

Mining stocks and M&A activity

This resurgence in gold's value also has a significant impact on mining stocks. As it rises, mining companies often see their share prices increase reflecting the enhanced profitability and financial stability brought with higher gold prices. With inflation currently under control, the upside potential for mining stocks becomes more apparent. The historical lag between gold price increases and mining stock valuations is expected to finally narrow whilst the positive correlations should once again reach higher levels. Whilst gold has recently reached historic highs (2’450 USD in May 2024), mining stocks are still, on average, 60% below their peak. This scenario presents a promising outlook for mining stocks.

This is evidenced by significant, large-scale M&A activity in the gold mining sector. They have occurred at the pace of approximately one transaction per year in the recent past. Examples include the Newmont acquisition of Newcrest in 2023, the Agnico-Eagle and Pan American Silver acquisition of Yamana Gold in 2022, the Newmont acquisition of Goldcorp in 2019 and the Barrick Gold merger with Randgold in 2018.

The strategic importance of gold

Smaller companies are not lagging either, with a significant number of consolidations as well, as exemplified by the activity of the first six months of 2024 which include the recent following acquisitions: Goldsource Mines by Mako Mining, Argonaut Gold by Alamos Gold, HighGold Mining by Contango ORE and Timberline Resources by McEwen Mining. Although mergers and acquisitions are theoretically value-creating, this has yet to be reflected in stock prices, leaving room for potential price appreciation. The divergence can be attributed to rising exploration and operational costs alongside environmental regulations and political considerations. Nonetheless, with inflation "under control" and regulations “under review”, the potential appreciation in mining stocks should become more evident.

The importance of gold in our economy is again becoming strategic, as the dominance of the USD seems to be weakening alongside other FIAT moneys. This emphasises the dynamic relationship between gold prices and the mining sector, including M&A trends.

At APIS, we welcome this opportunity and intend to leverage our expertise in managing our funds that invest in gold and silver mining equities. These funds are poised to benefit from, amongst others, current geopolitical tensions, gold acquisitions by central banks and Asian countries, the disparity between precious metal mining equities and rising gold prices, 20-year low gold mining stock valuations, producers increased margins and a historically lower than 1% global assets allocated to gold.

APIS Asset Management is a privately owned Luxembourg based UCITS and AIFM Management Company that has specialised in commodities funds over the last decade.

Link to the article published by Paperjam : https://en.paperjam.lu/article/gold-the-new-diamond-of-mining

Lien vers l’article publié par Paperjam : https://paperjam.lu/article/or-comme-nouveau-diamant-valeu

La mixité, un atout pour l’entreprise

Au Luxembourg, le nombre de femmes à des fonctions dirigeantes progresse lentement. Pour ces dernières, il est crucial de casser les croyances selon lesquelles il est impossible de concilier vies privée et professionnelle et de démystifier l’impact du temps partiel sur leur évolution au sein d’une entreprise. Une démarche que Sandra Lucente et Michèle Berger portent à bras le corps.

Au Luxembourg, le nombre de femmes à des fonctions dirigeantes progresse lentement. Pour ces dernières, il est crucial de casser les croyances selon lesquelles il est impossible de concilier vies privée et professionnelle et de démystifier l’impact du temps partiel sur leur évolution au sein d’une entreprise. Une démarche que Sandra Lucente et Michèle Berger portent à bras le corps.

Si, dans les comités de direction, le nombre de femmes tend à augmenter, marquant ainsi une évolution positive, au sein des conseils d’administration, leur présence est encore sporadique.

«Le pourcentage de femmes à des postes importants au sein de comités reste faible. Une marge de progression est possible. Il serait toutefois erroné d’affirmer que seuls les hommes sont frileux à l’arrivée de collègues féminines à ces postes. Je suis convaincue que certaines femmes intègrent malgré elles la croyance selon laquelle il est impossible de conjuguer vie de famille et vie professionnelle et que, dès lors, il faut choisir», explique Sandra Lucente (CEO d’APIS ASSET MANAGEMENT).

Pour encourager cette présence féminine, un changement de mentalité doit s’opérer chez chacun(e).

«L’effet de levier doit être mené conjointement tant par la gent masculine que par la gent féminine. C’est aussi notre responsabilité de femme d’exprimer notre envie d’évoluer. Dans le secteur financier, nous constatons qu’un effet pyramidal persiste, où le nombre de femmes reste plus important à la base et diminue au sommet. La situation va changer pour davantage de mixité et de complémentarité, mais de manière progressive», commente Michèle Berger (Présidente du Conseil d’Administration d’APIS ASSET MANAGEMENT).

Mettre fin à cet effet de pyramide

Créée en 2016 (sous le nom de IW Partners), APIS ASSET MANAGEMENT est une jeune société de gestion pour les fonds UCITS et les fonds d’investissement alternatifs (AIF). Possédant initialement un unique produit sous gestion, un fonds maison investissant dans les mines de métaux précieux, APIS ASSET MANAGEMENT décide de changer de stratégie.

«Ce changement s’est accompagné d’une définition plus claire de nos valeurs: l’expertise, mais aussi une certaine fraîcheur dans les services proposés. À travers cette idée de fraîcheur, nous désirons nous libérer d’une manière désuète de penser les problèmes et de trouver des solutions», précise Sandra Lucente.

APIS ASSET MANAGEMENT a, dans ce contexte, repensé la composition de son conseil d’administration et de son comité de direction en mettant des femmes à la tête de ceux-ci.

«Il s’agit d’un double signal. Nous avons, d’une part, désiré apporter des perspectives différentes pensées par des femmes dans des fonctions stratégiques de la société pour introduire davantage de fraîcheur dans nos services. Nous souhaitions également montrer la place que la femme peut avoir au sein des secteurs professionnels et ses capacités à concilier différentes vies: privée et professionnelle.»

Mener plusieurs vies de front